an accountant made the following adjustments at december 31, the end of the accounting period:\nc. unearned…

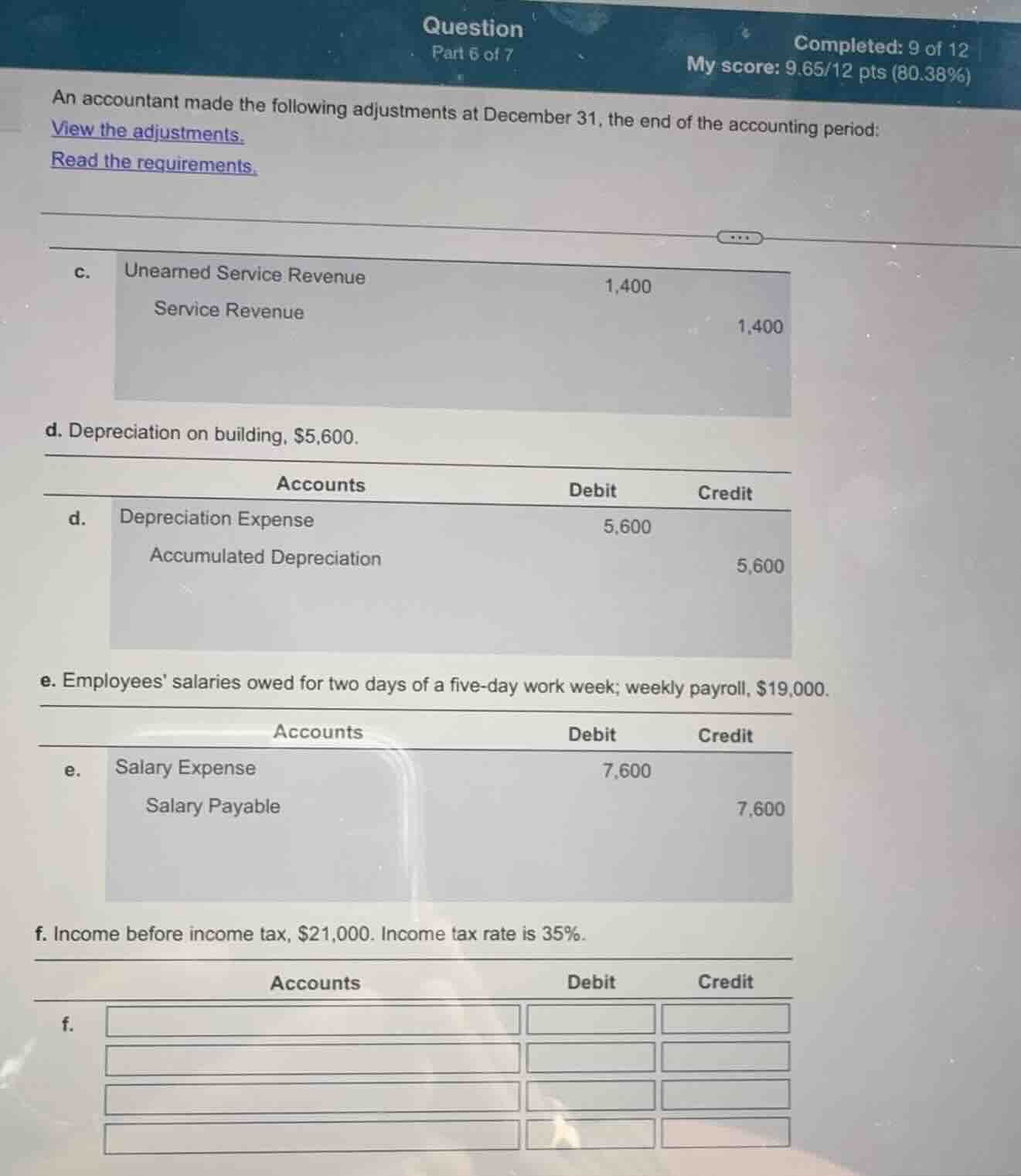

an accountant made the following adjustments at december 31, the end of the accounting period:\nc. unearned service revenue 1,400\nservice revenue 1,400\nd. depreciation on building, $5,600.\naccounts debit credit\nd. depreciation expense 5,600\naccumulated depreciation 5,600\ne. employees salaries owed for two days of a five-day work week; weekly payroll, $19,000.\naccounts debit credit\ne. salary expense 7,600\nsalary payable 7,600\nf. income before income tax, $21,000. income tax rate is 35%.\naccounts debit credit\nf.

Answer

Explanation:

Step 1: Calculate income tax expense

$$21,000 \times 35% = 7,350$$

Step 2: Identify accounts for adjusting entry

Debit Income Tax Expense and credit Income Tax Payable.

Step 3: Record the journal entry

Debit: Income Tax Expense $7,350; Credit: Income Tax Payable $7,350.

Answer:

| Accounts | Debit | Credit |

|---|---|---|

| Income Tax Expense | 7,350 | |

| Income Tax Payable | 7,350 |