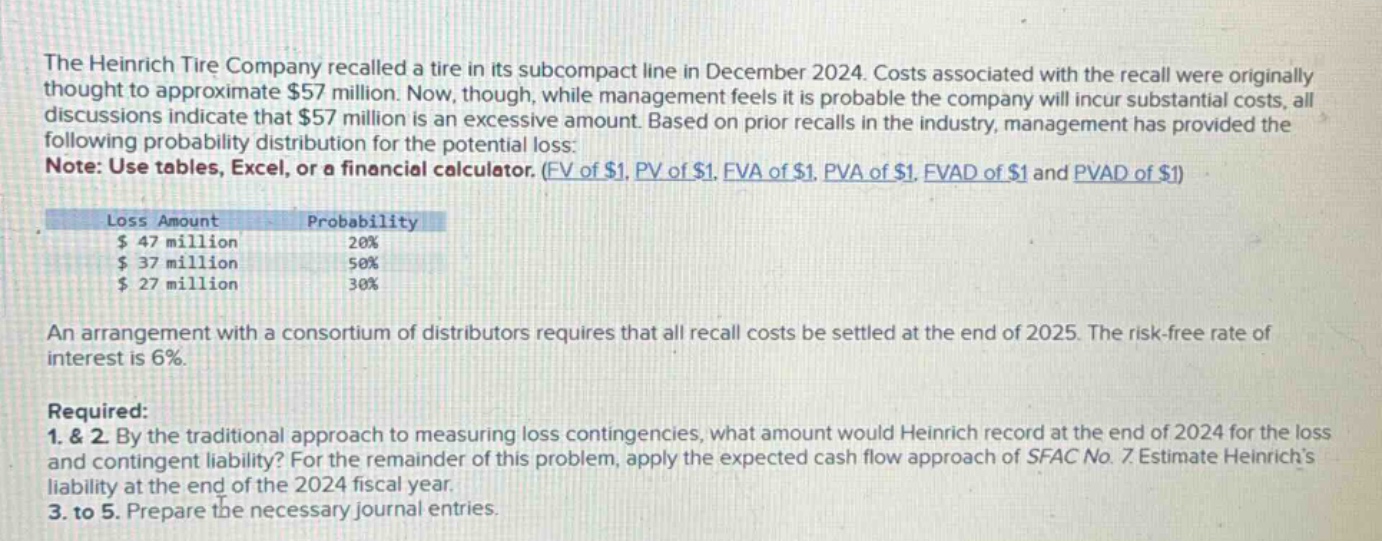

the heinrich tire company recalled a tire in its subcompact line in december 2024. costs associated with the…

the heinrich tire company recalled a tire in its subcompact line in december 2024. costs associated with the recall were originally thought to approximate $57 million. now, though, while management feels it is probable the company will incur substantial costs, all discussions indicate that $57 million is an excessive amount. based on prior recalls in the industry, management has provided the following probability distribution for the potential loss: note: use tables, excel, or a financial calculator. (fv of $1, pv of $1, fva of $1, pva of $1, fvad of $1 and pvad of $1) loss amount probability $ 47 million 20% $ 37 million 50% $ 27 million 30% an arrangement with a consortium of distributors requires that all recall costs be settled at the end of 2025. the risk - free rate of interest is 6%. required: 1. & 2. by the traditional approach to measuring loss contingencies, what amount would heinrich record at the end of 2024 for the loss and contingent liability? for the remainder of this problem, apply the expected cash flow approach of sfac no. 7 estimate heinrichs liability at the end of the 2024 fiscal year. 3. to 5. prepare the necessary journal entries.

Answer

Explanation:

Step1: Calculate expected cash - flow using traditional approach

The traditional approach for a loss contingency when it is probable and the amount can be reasonably estimated is to use the most likely amount. Here, the probability of a $37$ million loss is $50%$ (the highest probability). So the amount to be recorded for loss and contingent liability using the traditional approach is $37$ million.

Step2: Calculate expected cash - flow using expected cash - flow approach

The expected cash - flow formula is $E(X)=\sum_{i = 1}^{n}x_ip_i$, where $x_i$ is the loss amount and $p_i$ is the probability. $E(X)=(47\times0.2)+(37\times0.5)+(27\times0.3)$ $E(X)=9.4 + 18.5+8.1$ $E(X)=36$ million

Since the costs are to be settled at the end of 2025, we need to discount this amount back to the end of 2024. The present - value formula is $PV=\frac{FV}{(1 + r)^n}$, where $FV$ is the future value, $r$ is the interest rate, and $n$ is the number of periods. Here, $FV = 36$ million, $r=0.06$, and $n = 1$. $PV=\frac{36}{1 + 0.06}\approx33.96$ million

Step3: Journal entries

For traditional approach (end of 2024)

Debit: Loss from Recall $37$ million Credit: Estimated Liability for Recall $37$ million

For expected cash - flow approach (end of 2024)

Debit: Loss from Recall $33.96$ million Credit: Estimated Liability for Recall $33.96$ million

Answer:

- Traditional approach amount: $37$ million

- Expected cash - flow approach amount (discounted): $$33.96$ million

- Traditional approach journal entry: Debit: Loss from Recall $37$ million Credit: Estimated Liability for Recall $37$ million

- Expected cash - flow approach journal entry: Debit: Loss from Recall $33.96$ million Credit: Estimated Liability for Recall $33.96$ million

- (No additional information provided for fifth part in the question - assuming the above journal entries cover the requirements)